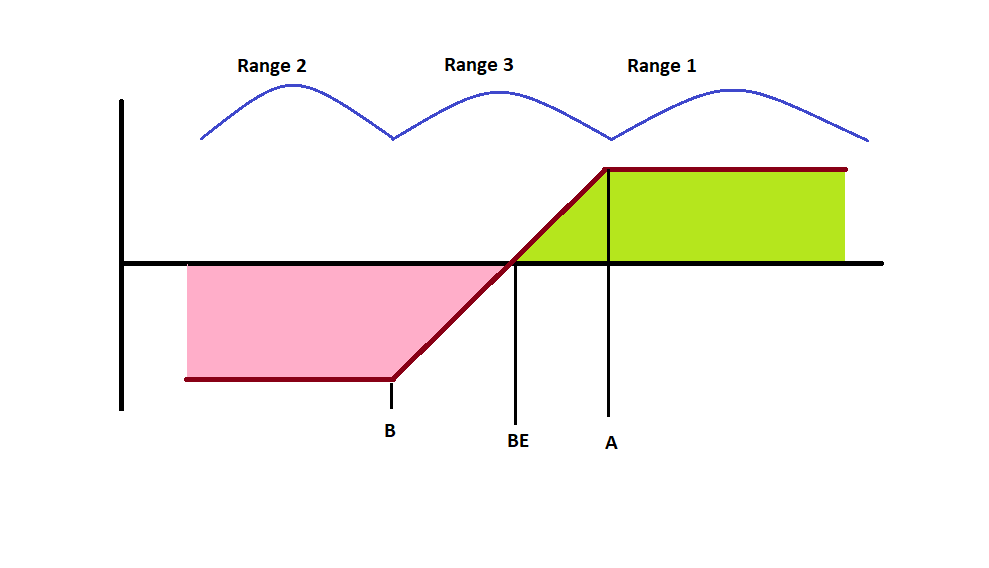

In the realm of trading strategies, Expected Value (EV) is a statistical measure that seeks to predict the potential profitability of a particular strategy,…

This is a multiple-article series. In part one, Implied Volatility backtest – Predicting IV Change, we discussed how the IV percentile predicts future IV…

Implied Volatility backtest – Predicting IV Change

[We have just added another article in the series, about the Real Volatility (or Historical Volatility) backtest. Check it at Implied Volatility Backtest 2:…

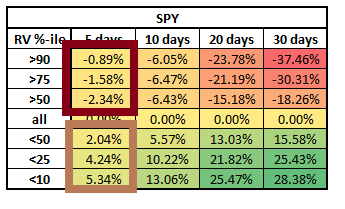

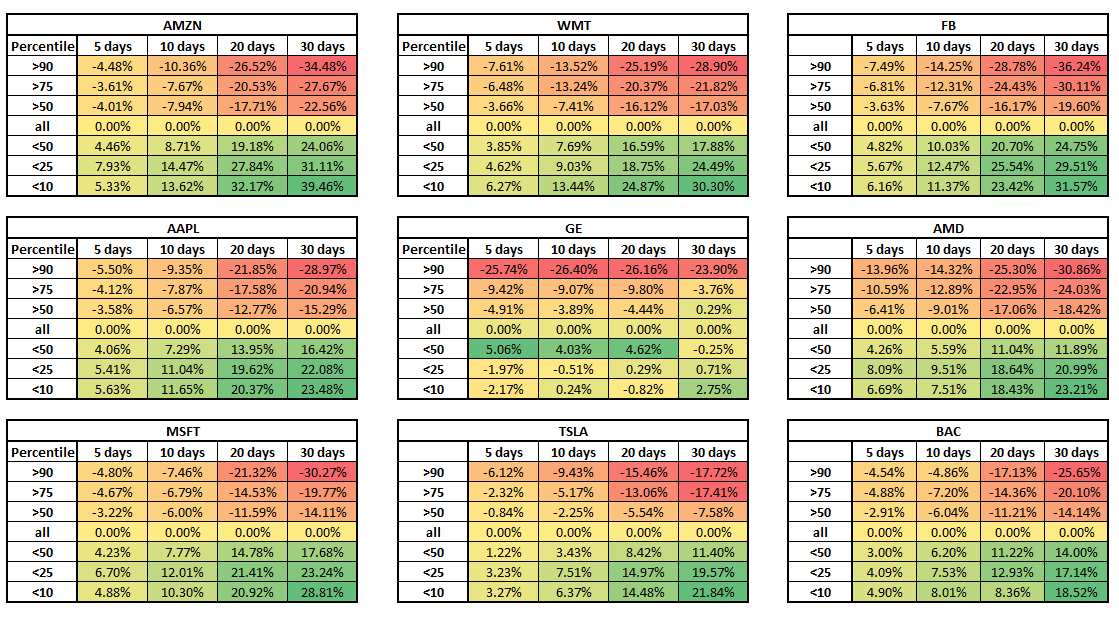

Many traders ask themselves how much the Implied volatility drop after earnings. Since earning release are very volatile – We can see an increase of IV…