Recently $JPM had its investor day and shared vast amount of information with its holders (link). I feel that the bank shared a lot of information emphasizing its power and value. The investor day itself was very long. But you can see a good summary here. Since I’ve already explained my position regarding JPM warrant, in this post I wish to highlight the most important slides (for me, at least) from JPM presentation.

You can read and download my valuation model for JPM warrants here.

Investors day highlights

Since I have already described my view about JPM, and provided a model where you can test your own assumptions, I’ll keep it brief. The best slides in the investor day were:

Book value growth:

We can see that book value grew each year – even during the financial crisis. The bank did not show loss.

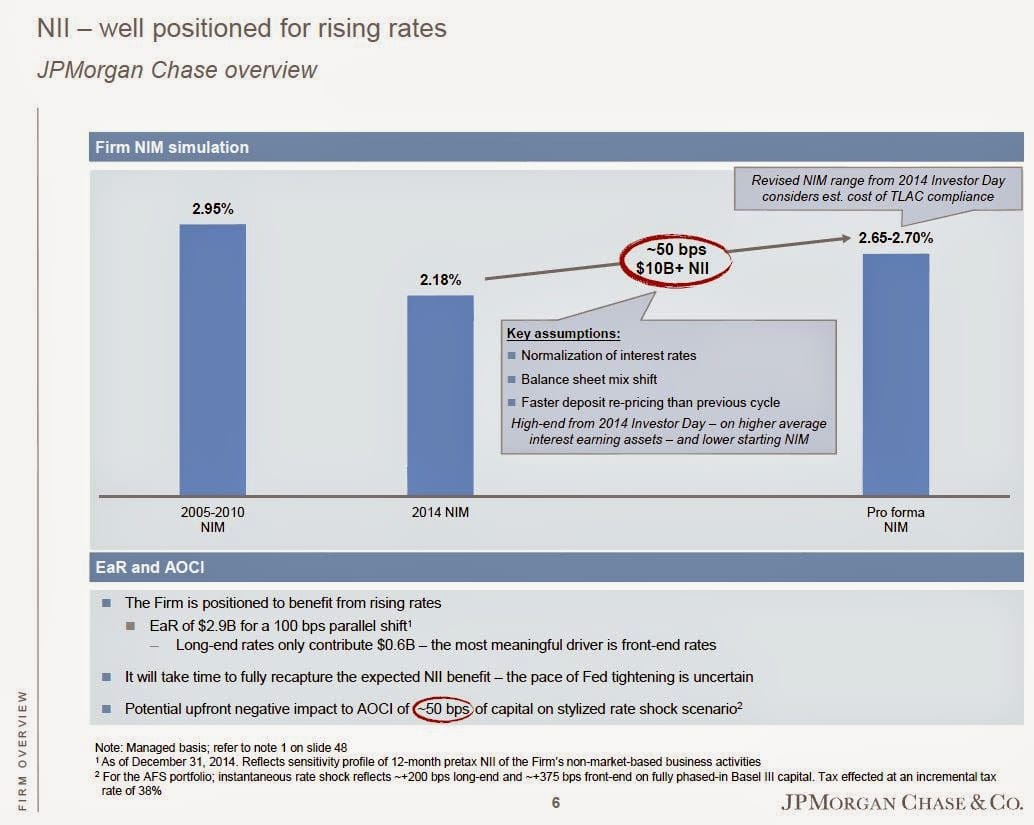

Interests rates:

Sooner or later interest rates would rise. It looks like the bank is well suited for this scenario as it will increase its gains.

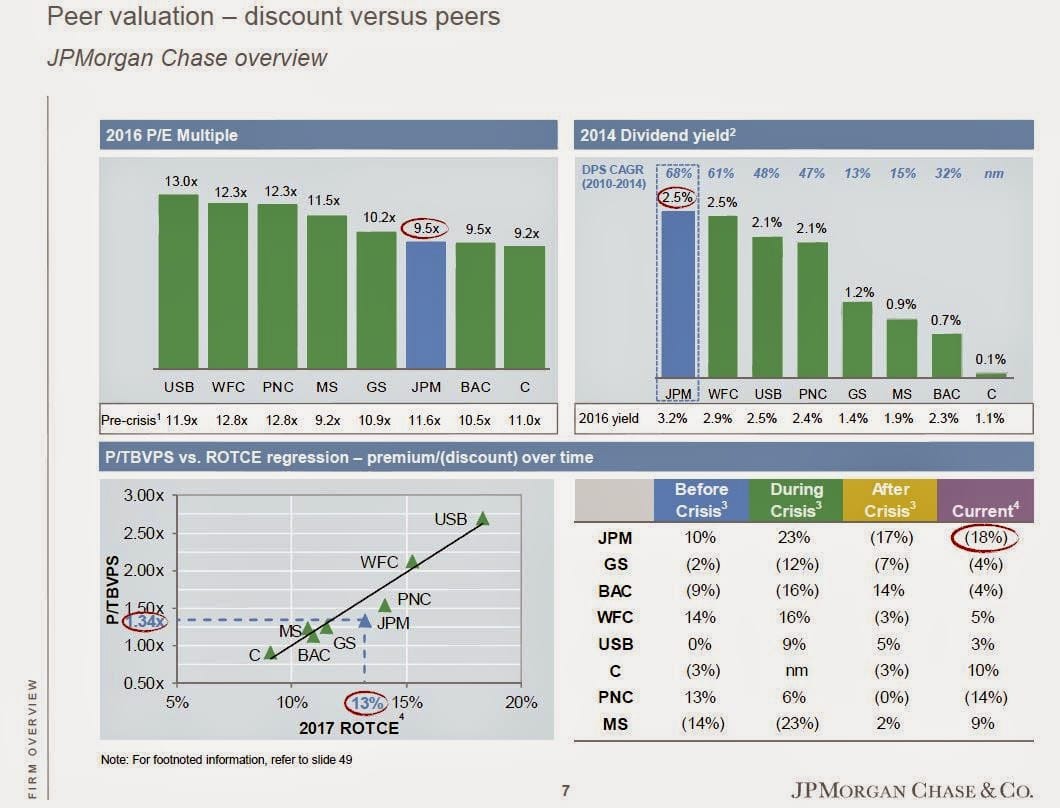

Valuation:

Though this is one of the strongest banks in the system, it is among the cheapest of its peers.

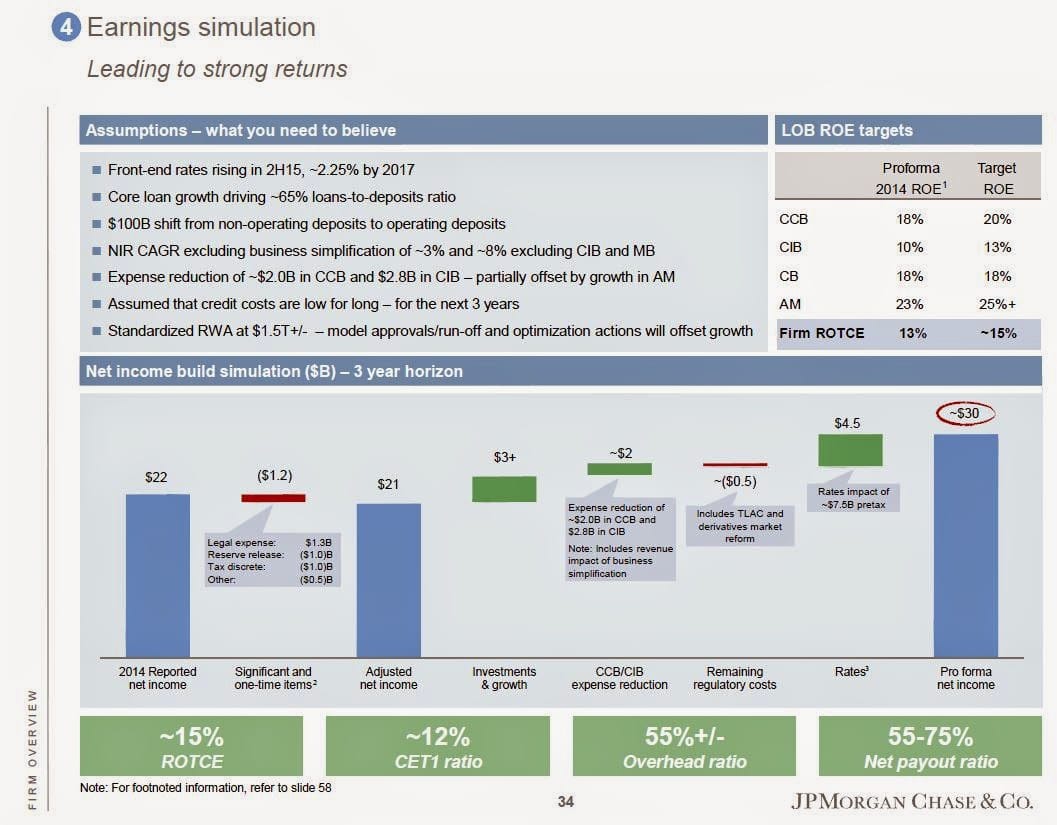

And most importantly – EPS growth:

$JPM management expects a 32%~ EPS growth in 3 years. In my model I assumed 7% per year and got that the warrants could triple (read here). JPM’s scenario would yield much better results. Another valuation from Brooklyn investor :

JPM sees net income of $30 billion by 2017 (or I should say JPM will have earnings power of that much). In 2014, there was $1.1 billion in preferred dividends paid and $544 million of “undistributable earnings allocated to participating securities” between the net income line and net to common shareholders. So that takes net to common down to $28 billion or so. With 3.7 billion currently outstanding (which may go down from repurchases), that’s $7.57/share in EPS. At a pre-crisis P/E of 12x, JPM can be worth $91/share. JPM is now trading at around $61/share.

The valuation above expects JPM to reach $91 by 2017. In my model, I assumed that price by 2018 (but I used a lower growth rate). I feel that my model is conservative and even with current stock prices and warrant price (19$~) I still see more than 150% upside.

You can find the best trade for this in our Options Screener. It has a scenario analyzer that optimizes the best options trade for each strategy.

Summary

JPM is one of the better banks in the system that managed to show consistent profits in recent years. The bank distribute dividends and is one of the cheaper banks when compared to its peers. More importantly – The bank is will be able to handle rises in interest rates when they occur, and might increase its profit. Lastly, The warrants allow us to leverage the position cheaply.

Read more about the PayPal and eBay infographics we’ve created.

* Please note that I’m long $JPM. My analysis offered here is not intended as advise and might contain errors.