This is a long thesis for JPM TARP warrants. The idea is similar to the previous thesis I gave on WFC here. JPM is one of the “big four” banks in the US. It is a full-service bank, with a huge market share and profitable divisions in all banking sub-sectors, such as trading, investments, credit cards, loans, mortgages, etc. The Warrants are long-term options to buy a JPM stock at $42.377. The option is currently in the money and offers a leveraged position till expiration – Oct 2018. Please note that at this date, the option will expire and become worthless so you have to assign it or sell it before.

JPM Stock

Long term look at $JPM shows that the stock broke out of the 42~ price line in 2013 and has been in a clear up trend since. We can see that recently the company gaped down after missing earning estimates.

And daily prices:

JPM had an average estimate for Q4 profit of $1.3. the reported EPS was $1.19 – $0.11 lower than estimates. This caused the stock to fall. The report was not bad, though and the company still has significant upside. In the following paragraph I’ll explain, briefly, the results and my outlook at the company.

Was Q4 earning that bad?

The fourth quarter results missed wall st. estimates. But JPM is a huge bank and it is impossible to say that results were all bad. The bank has problems in the legal aspects and legal expanses for Q4 were more than $1 billion (!), and it has some problems with mortgages. But the bank showed some great trends in its core businesses:

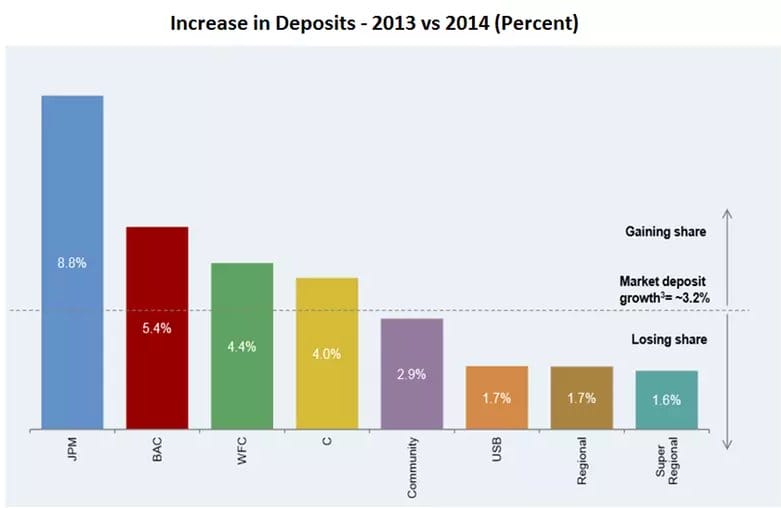

The bank is #1 in new deposits among the big banks in the US:

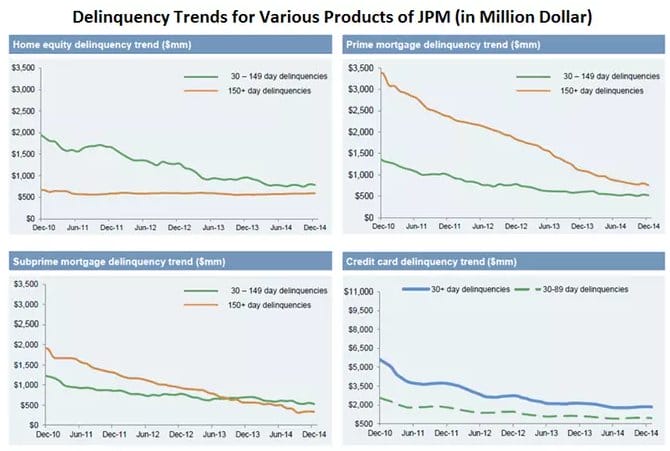

Delinquency rate is trending down:

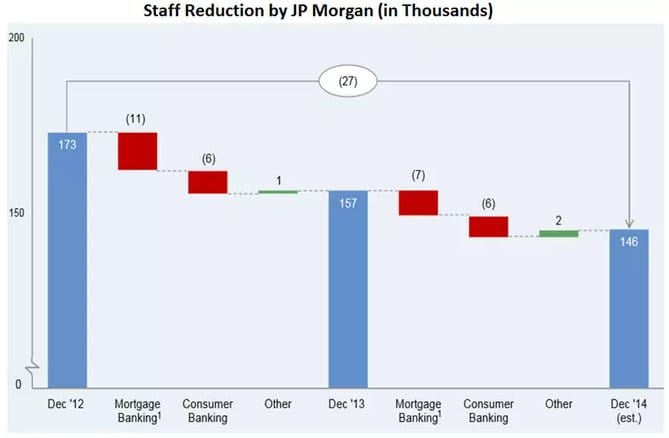

And the bank is continuing to improve costs:

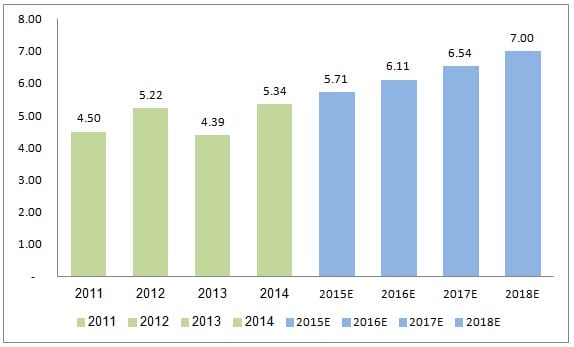

Overall, Despite sales decrease, the bottom line increased:

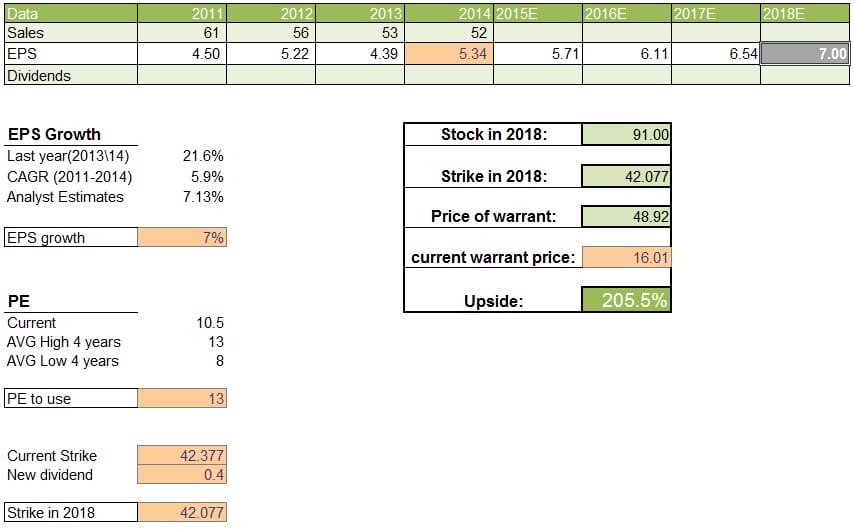

The EPS is 5.34$ per share, the highest the bank achieved, and the PE ratio – 10.5 – is low (the above projection assumes 7% EPS growth).

Since I think the legal problems are temporary and I think the bank brand will help it, not only keep profitability but increase market share, I think buying the warrant (or stock) will be profitable.

You can use Option Samurai’s options screener and trade optimizer to find the best way to trade this outlook.

The JPM warrants

Since I think buying JPM will be profitable, I like taking a position in JPM warrants. As I said, the warrants are call options with strike price of $42.377 – which means you can trade a warrant for JPM stock for 42.377 till expiration (Oct 2018). I would rather build my position in the warrants and not the stock because of Leverage – Since the strike is $42.377, the JPM warrants is traded for about $16, compared with 56$ of the stock price. A move of 1% in JPM will change 56 cents. Since the option is in the money, it will also rise by about 56 cents. But this move represents a higher percentage move – 3.5% (0.56/16). This means that you can gain about 3.5 leverage on the position, with a very long option.

Valuation of JPM warrants

Similarly to my WFC thesis, I’ve included an excel model, where you can adjust and see a projected value for the warrant.

My assumptions:

- 2014 eps is 5.34$ (reported)

- EPS growth 7% – Similar to analyst predictions (I think JPM could surprise to the upside)

- PE in 2018 – 13 (compared with 10.5 now)

- Adjusting the strike price 0.1$ per year due to dividends (I think it’s conservative)

Under these assumptions, I think JPM will be around 91$ by the end of 2018 and that the warrant will be priced at about 48.92 – 200% more than today.

I think that this model is possible – especially as it’s a continuation of current trends, without accounting for possible upsides from less litigation, spin-offs, increase in margin, etc.

JPM vs WFC Warrants

I’ve written previously about WFC warrants. I think that the thesis is still valid after the Q4 release. If I try to distill and summarize the thesis:

- WFC is the more conservative bank, looks to me safer, and offers an upside of 100% in the warrants.

- JPM is a great bank, with more risk, but the reward can be more than 200%.

* I have a position in both banks and the bigger one is in JPM.

You can download the excel model here: OS-JPM Model

- Check our public trade log – a performance chart and an update.