Update: This article describes what vertical spreads are, considerations on how to build optimal spreads, data points to take into considerations, how to find your comfort zone, and more. Feel free to ask us questions and try our option scanner that does all of it for you.

INTRODUCTION

Vertical spreads are perhaps the most fundamental option structures besides the single calls and puts. A trader can be profitable just purely by trading strategies using only vertical spreads. If you wish to, you can also take vertical spreads and construct more advanced structures that fit your style and market outlook. Therefore, it is especially important that a trader is well versed in some technical details behind the construction of a good vertical spread.

There are several approaches to construct a good vertical spread. If you do not have a specific market direction bias, you can make use of the expected move factored into the options pricing to find strike prices that give you a high probability of winning that trade. You can also create vertical spreads on underlying only when the IV rank is at an elevated level.

A vertical spread can be constructed to take advantage of your directional bias in the market by factoring in support and resistance, together with the expected move. When you structure a vertical spread this way, there are some guidelines to consider, ensuring that you are not overpaying for it. If you are an advanced trader, you can also investigate the volatility skew to find optimum strikes for your vertical spread. In this article, we will discuss these matters in detail with the exception of volatility skew.

A QUICK RECAP: WHY VERTICAL SPREADS?

Single calls and puts can be expensive and vertical spreads can be considered as an “extension” to reduce the buying power and in some cases to provide a hedge.

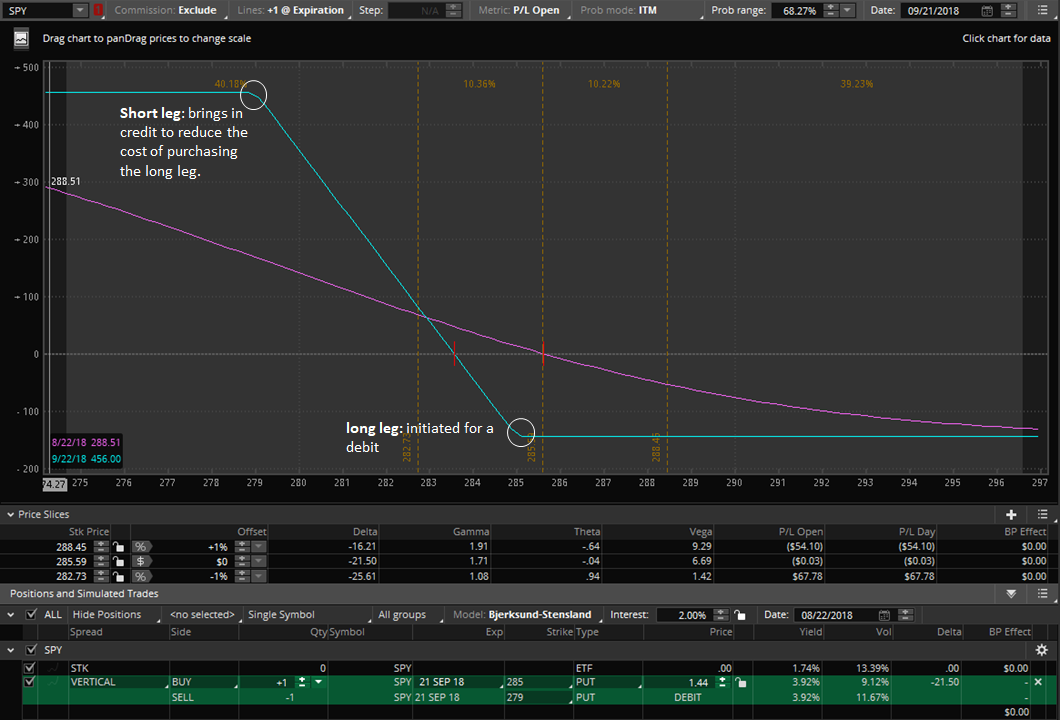

A short vertical spread is a short option position (credit) with an additional long position (debit) to act as a hedge. The net effect is a credit received on opening that spread. A short vertical spread has a significant reduction in buying power compared to a naked short position (because of the limited loss baked into the position). This is one advantage of vertical spread.

Short Vertical Spread

A long vertical spread is a long option position (debit) with an additional short position (credit) to reduce buying power. We can see the short position as a way to “partially pay” for the long position. The net effect is a debit on opening that spread. Similarly, the advantage of this vertical spread compared to a single long position is the reduction in buying power. In other words, it is a cheaper alternative.

Long Vertical Spread

FINDING YOUR COMFORT ZONE

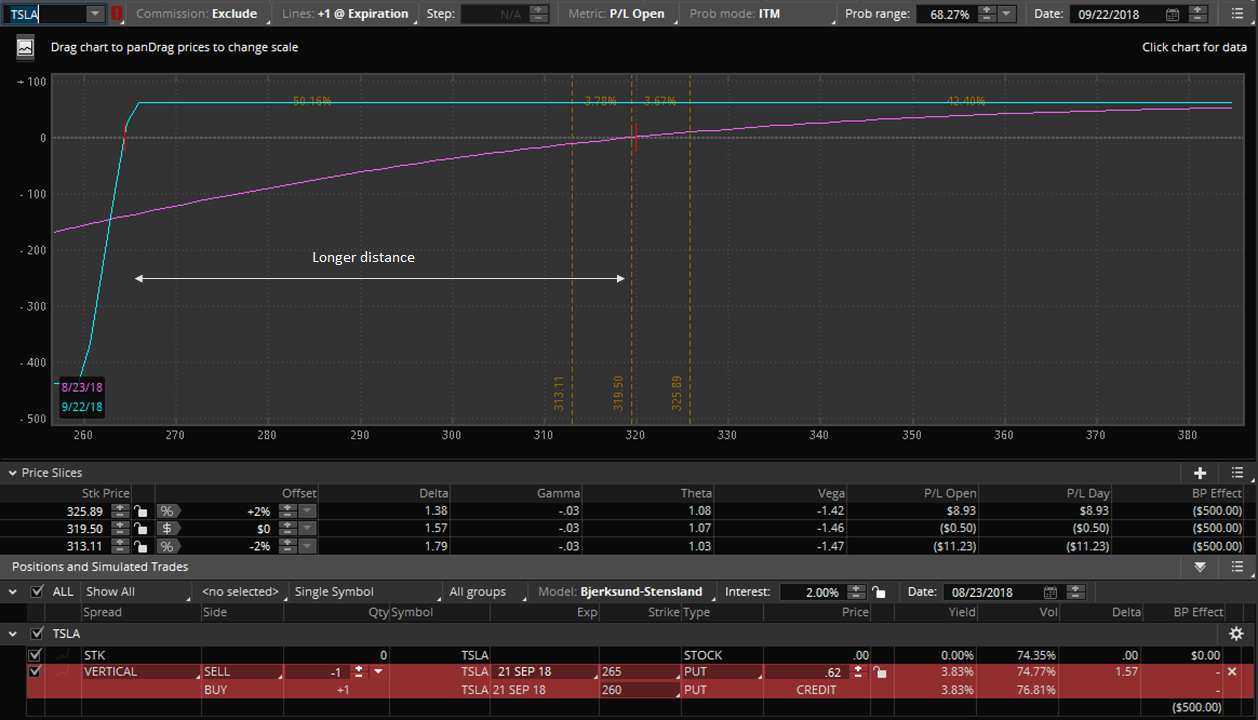

A common issue that many options traders face is the selection of the short and long strikes in a vertical spread. Where to place the short strike? After that where do I decide how far apart should the long strike be?

The answer, in short, is it depends on your comfort level. There are two inversely related outcomes when it comes to vertical spread. The probability of profit and Max Reward are inversely related. If you want a higher probability of success in your vertical spread, then you will have to settle for lower max reward and vice versa. You cannot have the best of both worlds unless you factor in trade adjustments and that requires another article for further discussion.

The probability of success, loosely speaking, is dependent on the position of your short strike. Let us consider the case of a vertical spread where the short strike that is far away from the at-the-money. This will create a trade with a higher probability of success but a lower amount of credit received. If the short strike is near at-the-money, the probability of success is lower but the total credit received is higher.

The long leg acts as a hedge for your short leg and it also controls the margin required by the sale of the short strike. The long leg will provide a hedge for the short leg but that will mean it comes with a cost resulting in a reduction of the total amount of credit received. If the long leg is near the short leg, the cost of this hedge will be larger and hence the credit reduction is larger but in exchange, the hedge is stronger and requires lower margin. The opposite is true. With the long leg further away from the short leg, the credit reduction is lesser but the hedge is weaker and hence the margin required is more.

Summary Table of Probability of Profit and Max Reward

SYNTHETICALLY SPEAKING

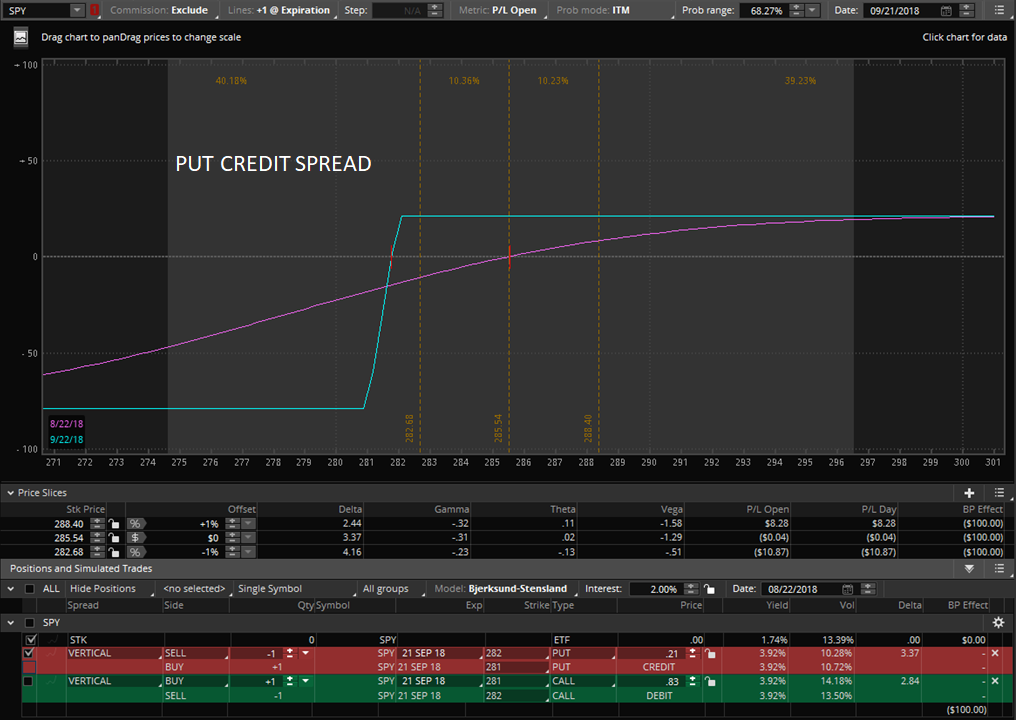

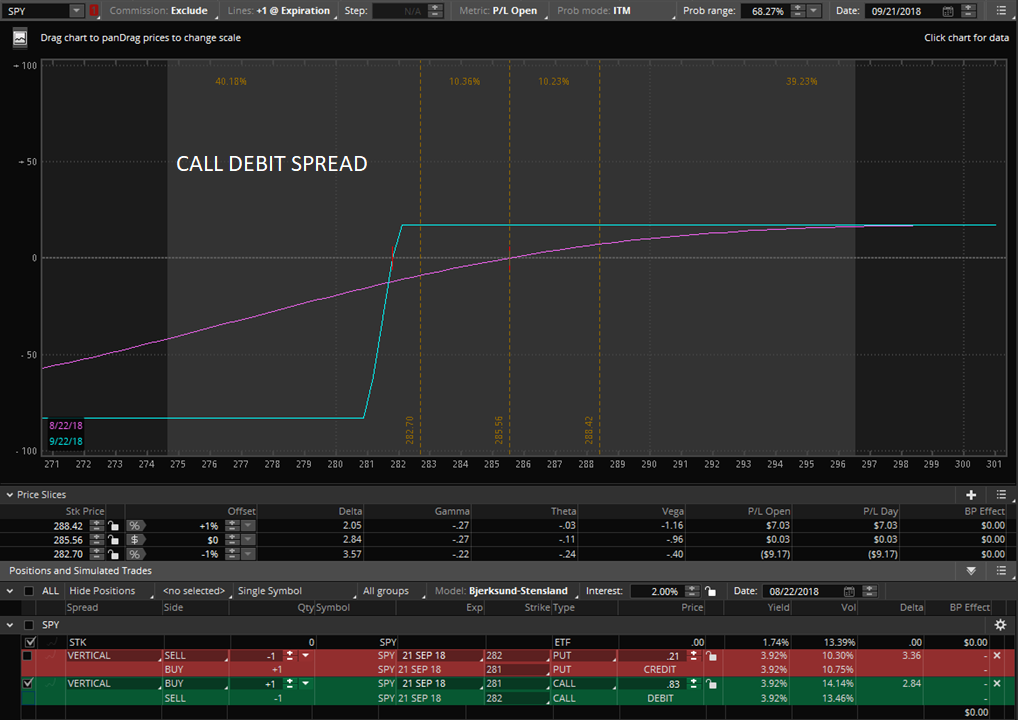

Short and long vertical spreads can be constructed to be synthetically equal. In other words, their risk graphs will look the same though they are constructed using different types of options (Puts and Calls). For example, a put credit spread is synthetically equal to a long call spread.

PUT CREDIT SPREAD

CALL DEBIT SPREAD (SYNTHETICALLY EQUAL TO PUT CREDIT SPREAD)

OPEN INTEREST COMPARISON

Parameters to build optimum vertical spread

If you are bullish on a stock and intend to do a short vertical spread, then selling out of the money put vertical spreads will be a better option than buying in the money call vertical spreads due to the liquidity issues as mentioned above. Similarly, if you are bearish on a stock, selling out of the money call vertical spreads will be a better option than buying in the money put vertical spread.

Bid-Ask Spread

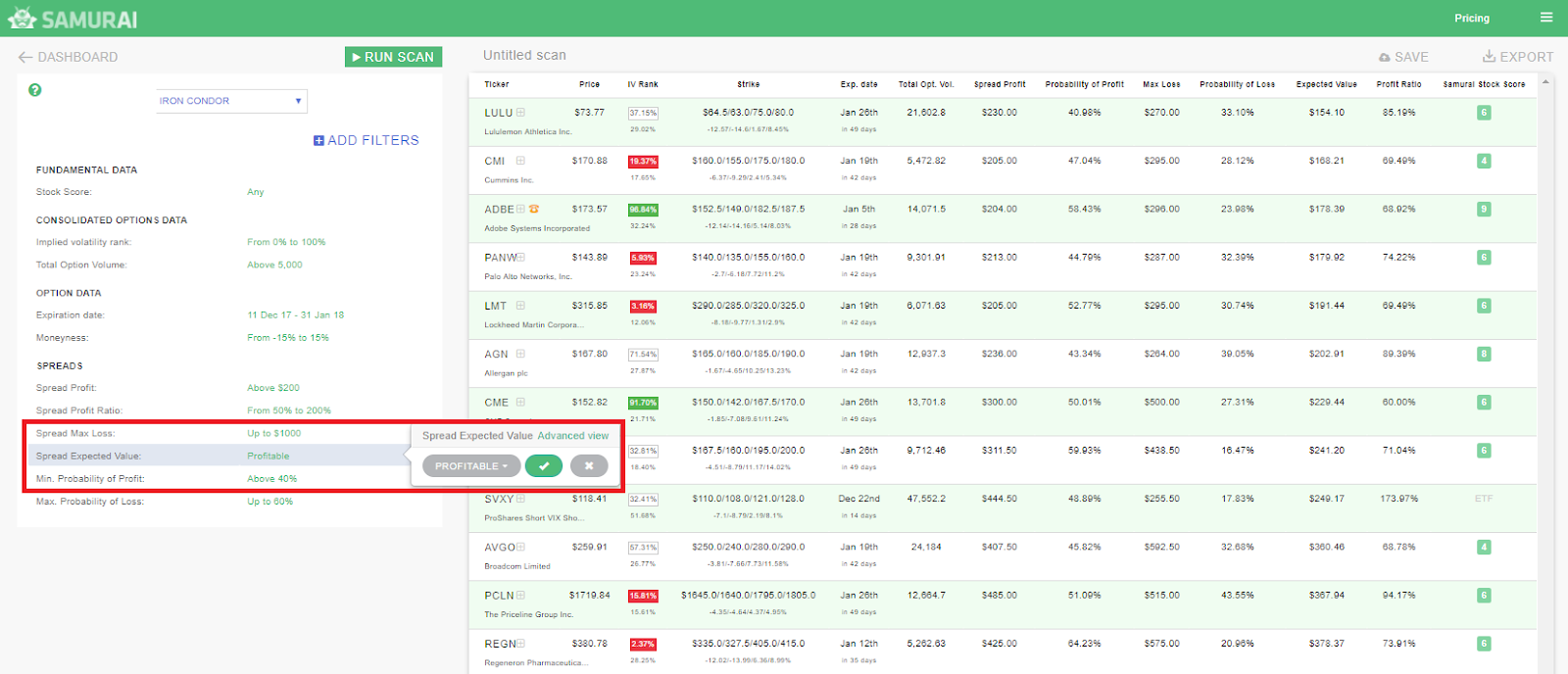

As a general guide, we want to buy and sell strikes that have a tight bid-ask spread. This can be achieved by looking out for strikes that have higher liquidity. Out of the money, strikes tend to have higher open interest and thus they provide more liquidity. In fact, our option scanner at Option SamurAI includes a filter that helps you zoom in on a tight bid-ask spread.

Bid-Ask Spread filter in Option SamurAI Scanner

EXPECTED VALUE

We always want the odds to be on our side. The best way to achieve that is to execute trades that have the best probabilities. The expected value statistically estimates the profitability of your option structure and by factoring market conditions, such as option prices, implied volatility, stock price, dividends and more to give a dollar amount of the expected profit (or loss) of the strategy. By factoring the expected move in the construction of your vertical spread, the expectancy of your vertical spread strategy will increase.

You can break up a vertical spread into three ranges as shown below.

Each range has its own

To calculate the expected value, we add:

- The probability of being above A * max profit (positive)

- The probability of being below B * max loss (negative)

- For the area between A and B, we use log-normal distribution and multiply it by the payout.

The sum of the three components is the Expected Value (EV).

You can also review the expected value article to have a more in-depth understanding.

Using Option Samurai can make sure your spreads have a statistical edge, and you can sort by maximum EV, thus optimizing the probability of profit/loss with the profit or loss.

THE IV RANK FACTOR

The IV rank is one of the most principal factors when trading. Some traders prefer to trade underlying with high IV rank. The option premiums are higher when IV is elevated. When you sell a vertical spread under high IV conditions, the credit received is higher. You are expecting the high IV to revert to its lower mean and when that happens, the value of the spread decreases quickly and you can make a profit quickly. High and low IV rank is a subjective thing but as a guideline, anything above 50% is considered to be in the high range and vice versa. We have ran backtests to demonstrate this point. Check them here: https://blog.optionsamurai.com/implied-volatility-backtest-predicting-iv-change/

Another key advantage of deploying vertical spreads on high IV rank underlying is the fact that your short strike can be positioned further away from at-the-money while retaining the same probability of profit as compared to the one with low IV rank.

Let us compare TSLA and LMT both having almost the same price (321) but of different IV ranks. With TSLA having a higher IV (82.04), the expected move of 55.84 is also larger. LMT has a lower IV (24.39) and thus a smaller expected move of 12.35.

TSLA expected move (55.84)

LMT expected move (12.35)

You can also see from the risk graph the difference in the distance between the short strike and at-the-money when IV rank is high compared to when it is low.

Higher IV Rank

Lower IV Rank

You can easily use the Option SamurAI scanner to find trades with your preferred range of IV rank.

FINDING THE ACCEPTABLE “PRICE”

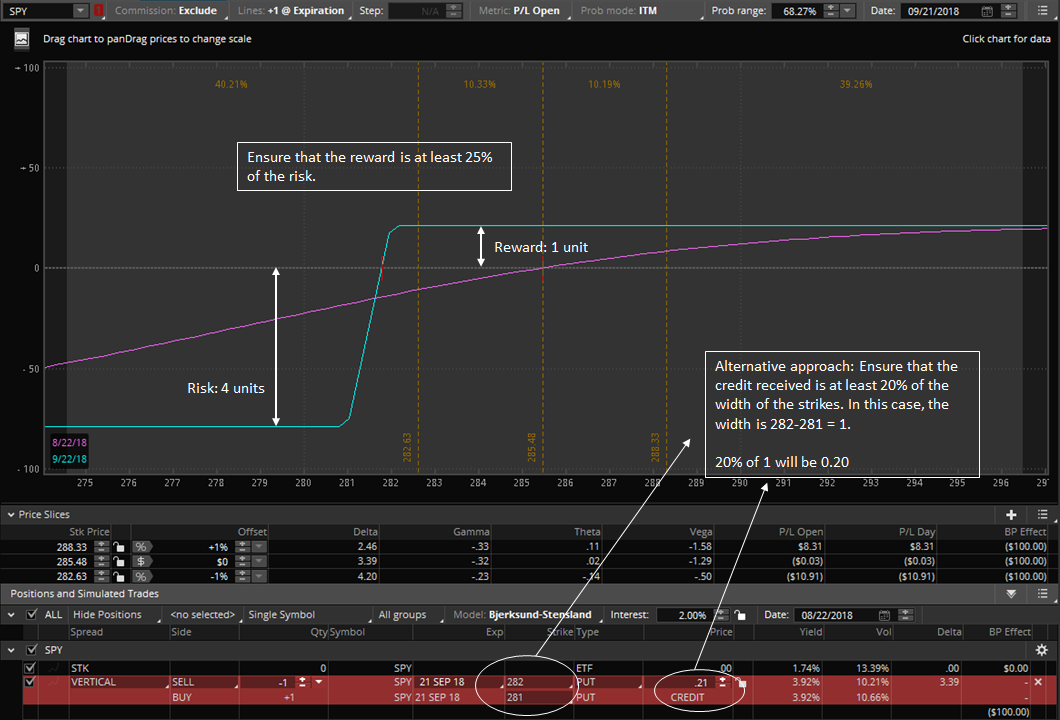

Some other traders prefer to use the relative pricing of the short and long leg as a consideration when it comes to the construction of a vertical spread. They ultimately want to create vertical spreads that come with reasonable “price tag”. If you belong to this category, you might want to consider the 25% guideline.

When constructing a short vertical spread, ensure that the reward is a least 25% of the risk. This is to establish a baseline for an acceptable reward to risk ratio of 1:4.

25% rule on the Short Vertical Spread

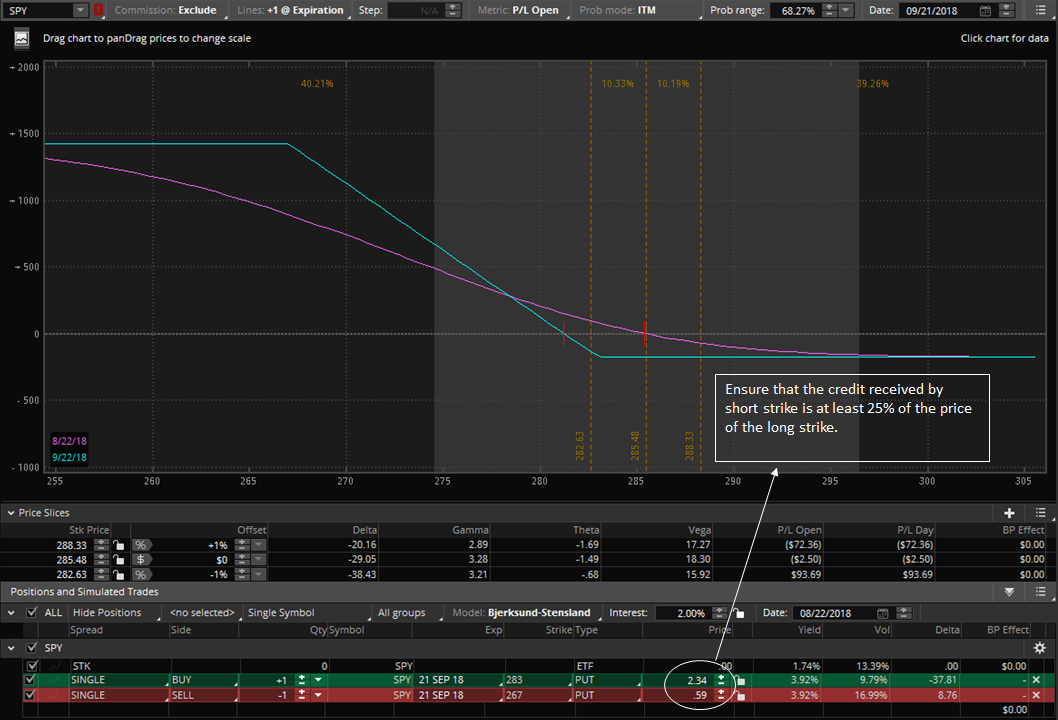

When constructing a long vertical spread, ensure that the short leg will pay for at least 25% of long leg. This establishes a baseline for an acceptable price for the spread.

25% rule on the Long Vertical Spread

NO STRONG DIRECTIONAL BIAS

When you do not have a strong directional bias, it is advisable to trade with the prevailing trend of the market and the individual stock. Alternatively, you can consider your entire portfolio and decide if you want to add long or short deltas to balance your portfolio (to be covered in future articles). You can use the expected move of the underlying as an estimate to position the short strike of your short vertical spread.

Assuming you have no directional bias on a stock but you wish to ride on the general bearish sentiment of the market, you can create a Short Call Vertical (Call Credit Spread).

You can filter out the best bearish call spread for the underlying by using the Option SamurAI scanner using the various factors discussed above.

Alternatively, If you wish to do this manually, the key thing is to position the short leg beyond the expected move.

- Determine the expected move to the upside.

- Position the short leg such that it is one strike away from the expected move. If you want a greater probability of profit, you can shift it even further away.

- You can find the long leg that can control the risk to your personal tolerable level and check that the reward to risk ratio is to your liking.

- Alternatively, you can consider the 25% guideline to position your long strike.

DIRECTIONAL BIAS

When you have a directional bias, it is still important to consider the expected move. However, you can factor in significant support or resistance levels to provide additional probabilities on your side and create vertical spreads with the short strike beyond that level. This is where you might want to consider creating the vertical spread from the “price” perspective.

Assuming you are bullish on a stock and stock has yet to bounce off a support, you can create an OTM Short Put Vertical (Put Credit Spread).

- You can filter out the best bullish put spread for the underlying by using the Option SamurAI scanner using the numerous factors discussed before.

Alternatively, If you wish to do this manually, the key thing is to position the short leg beyond the expected move. The key thing is to position the short leg within the range of appropriate strikes.

- Identify key support.

- Decide on the expiration cycle.

- Position the short strike below the support. It is even better if the expected move is larger than the distance between support and the current candlestick.

- Find the nearest long strike that can give you a vertical spread with reward to risk ratio of 1:4

- If the current expiration cycle does not provide you with the reward to risk ratio of 1:4, look at the next expiration cycle further out in time.

USING OTM DEBIT VERTICAL SPREADS

Assuming you are bullish on a stock and stock has already bounced off support, you can create an OTM long call vertical using the 25% guideline for long vertical spreads. It is important to note that a bullish OTM long call vertical spread is more aggressive than a bullish OTM short vertical spread as it doesn’t have positive theta and therefore you will need the stock to be moving in the right direction preferably right after the vertical spread is put on. That is why this is suitable when the stock has bounced off support as mentioned earlier.

PUTTING IT ALL TOGETHER

Let us do a case study on MS. This image was taken on 30 Aug 2018. Using the mean reversion concept, you can now consider a bearish call vertical spread.

You can see that MS is trading below its 200 SMA (red line) which is a long-term bearish trend. It is currently overbought (84.27) based on RSI(3 periods). Let us assume that MS will revert its movement towards the bearish mean.

You can now enter a Call Credit Spread. Consider the resistance lines in dotted yellow. If you are aggressive, you can position your shorts just above the 51 strike, which is the region of the lowest yellow resistance line. It also coincides with the 50 SMA (green) resistance line.

However, if you are less aggressive, you may want to position your short strike above the 52 strike, which is the region of the 52 resistance line.

If you are very conservative, you may want to position your short strike above the 55 strike, which is the region of the 55 resistance line.

IN A NUTSHELL

-

- You want to take advantage of expected moves and construct a high probability trade.

- Find your comfort zone, find your own sweet spot between the probability of success and max reward.

- Always trade on stocks with high liquidity, aim for tight bid-ask spread.

- Trade on stocks with high IV rank.

- If you are more conscious of relative pricing of the strike of the vertical spreads, consider the 25% guideline.

- Any approach you take is fine as long as it has a positive expectancy (you can use our Option Samurai’s scanner for that).

(Originally published on Sep 2018 and updated since)

[…] Build an optimal vertical spread […]